Navigating choppy waters: focus, execution & tenacity FTW

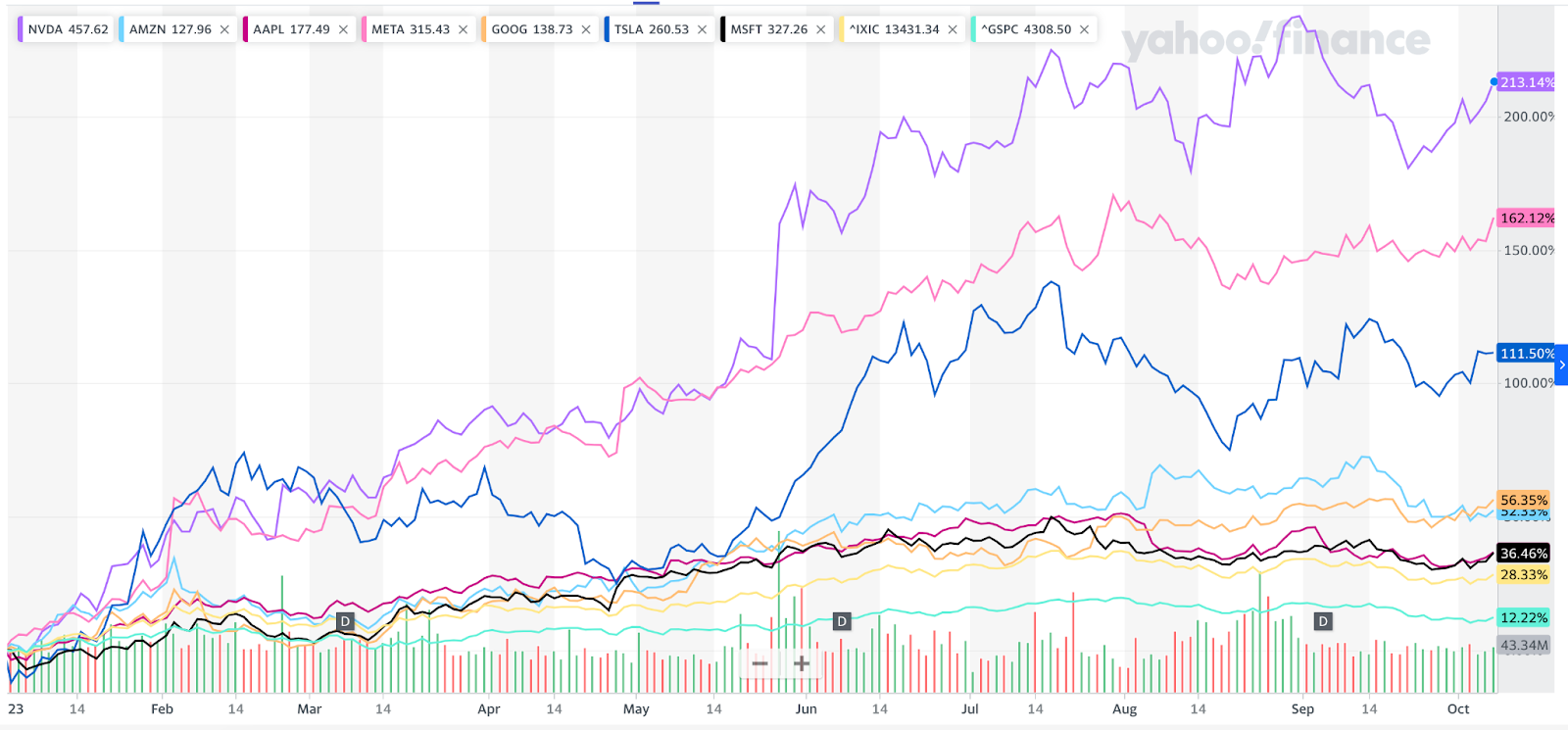

2023, although it’s far from over, has to date been a good year for publicly traded stocks. The S&P and Nasdaq are up ~12% and ~29% respectively year to date. Masked by the rise of these indices is the fact that most of that increase can be attributed to 7 stocks: the Magnificent 7.

Seven companies (NVIDIA, Apple, Microsoft, Alphabet, Meta, Amazon and Tesla) account for $3.7 trillion of the increase in market cap in 2023, and removing them from the S&P 500 and NASDAQ removes much of the increase in value you see in both indices. Aswath Damodaran - Market Bipolarity: Exuberance versus Exhaustion

In spite of the rise of public stock indices and many tech companies, I remain cautious about the near future. I fear that there will be more pain and lots of bumps on the road to a “recovery”. More so, the recovery will not materialize in the exuberance we witnessed during the heydays of ZIRP.

The reasons for my caution, especially for private venture-backed technology companies, are many.

Startups are shutting down, at an accelerated rate

The first data point is one recently surfaced by Carta which shows that the rate at which startups are shutting down is both at record levels and continuing to accelerate.

One data point that the report highlights is that the number of startups shutting down at the b-series and beyond is also at record levels. I suspect that this trend will continue well in 2024, especially with later-stage startups. Many of those last raised money in 2021-2022 and would be approaching the point in which they need additional capital. Only some will be able to raise.

Even startups that are quite far down the alphabet stage journey are encountering trouble. 34 startups that had raised a Series B or later shut down this year, up from 25 in 2022.” Source: The Data Minute

FCF or bust?

A year ago I wrote an article on how startups must evolve from the unicorn to a cockroach, especially for late stage companies. In that article, I wrote the following:

[...] there is one and only one choice for companies in that stage: financial independence. These companies have to dramatically adjust their cost structure, and growth aspirations, to attain positive cash flows (and FCF). This financial independence will come at the expense of tapering growth, which was historically inflated by free and abundant cash. The future growth has to be self-generated, even if the rate of growth is significantly lower.

A recent post from Andy Price of Artisanal - one of the industry’s leading exec retained search firms - indicates that we still have ways to go. This combined, with the dearth of capital will increase the likelihood of later stage companies shutting down or seeking a “strategic” exit. I expect more of this to happen in 2024.

Rates go up, yet valuations are still rich

Below is a 10 year chart of the 10yr treasury rate, which as of 10/6/2023 stands at ~4.7%. The 3yr rate is slightly higher at ~4.9%. The higher these rates go, the more expensive capital becomes. This increase in treasury rates pushes up the cost of capital which causes ripple effects such as depressing valuations, raising the cost of car loans and mortgages and making it harder for startups to raise capital. Why would one put their capital on speculative and high risk investments if they can get ~5% risk free?

Not only is capital more expensive now, and for the foreseeable future, but the level at which valuations has dropped isn’t commensurate with the observed increase in risk-free assets (US treasuries). More pain to come.

The current median multiple is ~5.7x. As a reminder - the average software multiple from 2010-2020 was ~7.8x, and the average 10Y over that same period was ~2.3%. Given those two data points alone I’d expect the median multiple today to be closer to 4x! Clearly the bond markets are saying something different than software valuations. The disconnect in rates and multiples is even more stark when we look at growth adjusted multiples (taking revenue multiples and dividing them by forward growth rates). The current median growth adjusted multiple is 0.39x which is actually greater than the long term average pre-covid of 0.28x (so 40% higher!). Pretty crazy to think about - growth adjusted multiples are near pre-covid all time highs (excluding 2020-2021 period) even though rates are as high as they’ve been since 2007 (and double what they were on average from 2010-2020). Source: Jamin Ball- Clouded Judgement 9.29.23 - Rates Keep Going Up

It’s not all doom and gloom

I alluded earlier to being cautiously optimistic and recognizing that there will be more pain ahead. The reasons for my optimism, beyond adopting a mantra of “this too shall pass” are numerous. They are all predicated on a few conditions though: a product that provides obvious value to customers and a winning culture.

There are far too many companies - across almost all enterprise software categories - chasing the same customer dollars and buyer personas. There simply isn’t enough time or money for most of these companies to build a sustainable business. The winners will be the (very very few) that are able to navigate a very crowded space by offering clear and obvious value to their customers.

The past decade has witnessed a rather comfortable and cushy environment for startup employees. Money, and perks, were plentiful and the talent race predicated that companies - large and small - compete on compensation and perks.

During the ZIRP (zero interest rate policy) era employees only had to spend a small fraction of their time doing actual work to somewhat justify their inflated salaries/titles because the free money made everything easy. OnlyCFO When “Culture” kills

Successful companies that are able to navigate the continued turbulence ahead will be the ones that out-execute their competitors. The ability to do more with less and not defaulting to hiring as a means to do “more” will be crucial. Scarcity drives efficiency (and margins), agility, speed and focus on what truly matters to customers and the business.

The very few that can operate successfully in this environment will benefit from the continued headwinds. Many of their competitors, especially venture funded ones, might not survive. Fewer competitors means hiring will become easier so will winning new business and capital will flow to these winners.

Epilogue

The picture for this article is intentional.

I grew up hearing and reading about the Ra Expeditions. My second cousin - Georges Sourial - was a member of the Ra I. That vessel ultimately sank a week before making it to Barbados. The team regrouped, redesigned their boat and set sail on Ra II ten months later. Ra II made the journey in 57 days.

If there was ever a story of navigating choppy waters, perseverance, courage, skill and tenacity that was it. The very same traits needed for companies to navigate this environment.