IPO dreams

Don't hold your breath

Joining a startup can be an exhilarating experience. It allows you to actively participate in building new products from the ground up along with building a company. The latter in my opinion being one of the more exciting and rewarding parts of the journey. There is also another motivating factor to joining a startup; wealth creation. When we think of wealth creation in startups, we typically envision a growing company, one whose valuation balloons (unicorns) culminating in a flashy IPO.

Just how common is that and is an IPO the only liquidity event for startups nowadays? In this article, I will be exploring these questions and navigating the landscape of both public and private (venture) markets. Most of this article, including all the charts, are based of this most excellent report by Michael Mauboussin & Dan Callahan @ Morgan Stanley

1- The public vs private market size

The first point of interest to us is to look at the overall market size for both public and private markets in the US. The public markets is simply the sum of the market cap of all publicly traded companies in the US of which there were ~3600 such companies as of year end 2019. Similarly, the size of private market, which are private equity (buyout) and venture capital firms, looks at the total of their assets under management (AUM).

It should come as no surprise that the size of public markets in the US dwarfs both PE and VC. The public market was ~80x bigger than the size of the VC market in the US.

Source: Mauboussin et al

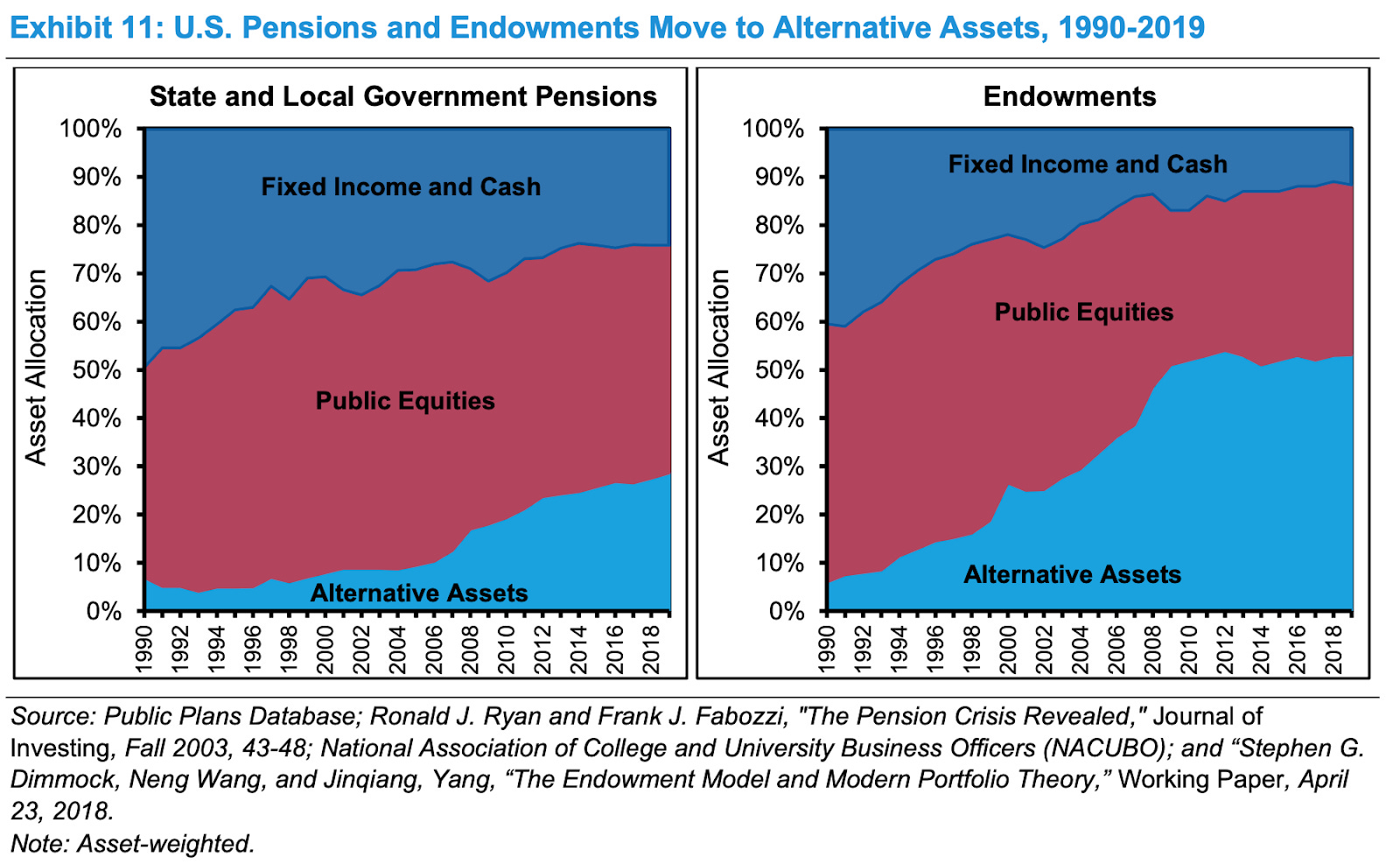

2- Where is the money going?

The next place for us to look at is to compare the flow of funds across various asset classes: cash, public equities (stocks) and alternative assets. The latter being the realm of VCs and Private Equity. The chart below shows a sizable shift from cash and public equities into alternative assets. Said otherwise, funds are moving from the public (stocks) into private assets (VC & PE).

From points #1 and #2 we now know that a) public markets are substantially larger than private ones and b) that the rate of funds flowing into private markets is accelerating. The acceleration being at the expense of cash and public markets.

3- Why the rush to private markets?

Returns.

Private markets offer better (risk adjusted) returns than public ones, as shown in the chart below. Observe the long right-tail of returns for both VC and buyout (PE) relative to that of public equities. Of interest as well is that 50% of VC returns lie anywhere between 0-1x of invested capital. VCs returns are dominated by very few very large winners.

If you are a large endowment or public pension fund you need to invest your capital to make meaningful returns in order to meet your future obligations. Private markets offer a good avenue to do so. The obvious caveat is that you have to be lucky or fortunate enough to be able to invest in the right funds

4- Which private assets to invest in?

We’ve seen that the returns from private markets are higher than those of public ones. We’ve also illustrated that the size of these markets relative to public ones is substantially smaller. Said otherwise, there’s a lot more money allocated in public equities that wished it would be allocated to private markets. There’s also another important factor in play. That of the persistence of returns.

The table below shows that VCs with top performing funds (top quartile) will also have their subsequent funds outperform their peers. Top VCs keep on winning.

The persistence of VC returns could be explained to better access to deal flow. Top VCs will tend to attract the best companies and entrepreneurs who want to work with them. Those companies will typically end up performing the best - a virtuous cycle ensues. Obviously, as an investor, you want to invest your money (or time if you are a founder or startup employee) with these top performing VCs.

5- How are VCs making $?

The next question for us to explore is to take a look at how VCs make $, or how do they realize their returns. I won’t be tackling any of the mechanics of what VCs do in terms of deal flow, evaluating where to invest and so forth. Instead, I will only look at how VCs convert their equity stakes in their portfolio companies into cash: how they exit.

The chart below offers the answer to this question. Nowadays, VCs will most likely exit from their portfolio companies by selling them (M&A) vs the IPO route. This is in stark contrast to pre-2000 where the most common exit was the IPO route. Nowadays, more than 90% of the exits are via the M&A route. Today, VCs are quicker to sell a business, often to an incumbent, than to wait and do an IPO

6- The IPO landscape

We now come to the crux of the article, which is to look at the overall IPO activity in the US. You can clearly see from the charts below that the level of IPOs (new lists) in the US peaked in the mid-90s and has been on a downtrend trend since then. In fact, the number of publicly traded companies in the US now stands at ~3700 down from ~7500 in the late 90s.

Not only are IPOs becoming exceedingly rare, but companies that do IPO take longer than ever to do so. The average age of a US company doing an IPO today is ~11 years vs ~8 historically.

But there’s more. Most of the value a firm creates is now whilst it is private. Google did an IPO 6 years after its start at a 30B market cap. Google’s market cap is presently ~1.1T. Similarly, Facebook went public 8 years following its founding with a market capitalization of $117 billion and today it’s market cap is ~800B. Virtually all of Amazon’s value has been created whilst it is a public company. Uber went public 10 years after founding with an initial market capitalization of $75 billion. Today, Uber’s market cap is ~$58B.

So why are companies staying private longer than ever now? Mauboussin offers a few main reasons which are outlined below.

First, is the cost and complexity of listing which has gone up since the Sarbanes-Oxley Act of 2002. Second, the motivation to go public has shifted. Young companies today don’t need to raise capital from the public market because they are generally less capital intensive than their predecessors. Today’s startup’s are CapEx light relative to companies in the past, especially in the software sector thanks in no small part to cloud service providers like AWS and Azure.

Third, even those companies that are in very competitive industries have been able to stay private because there is a huge amount of capital available via late-stage funds. Finally, there are now ways for employees who are compensated in equity to sell shares. In some cases, funding rounds give employees a chance to cash out. There are also private marketplaces now that enable employees to sell their private shares.

Putting it all together now

Back to the question posed at the top of this article on how common an IPO event is for a startup. It should be evident by now that it is quite unlikely that an early stage company will IPO. The M&A route is the more likely scenario. Unless off course the next few years show a change in this trend.

Regardless, joining a startup is not just because of the potential to create wealth. Startups offer many other advantages that can help accelerate your growth. We’ve covered a few of those in this article before. And, yes, an IPO or some sort of liquid exit is the icing on the cake!