Capitalizing R&D: What is it & its impact on software companies

No, it has nothing to do with CAPITALIZATION!

A few weeks ago I wrote a post covering some accounting principles that a VPE should familiarize herself with. It turns out there’s another accounting principle that will impact every software company. That topic is the capitalization of R&D costs. The reason this topic is growing in significance for both accounting and engineering departments has to do with the IRS.

In 2017 the Tax Cuts and Jobs Act was introduced. This act reduced the corporate tax rate from a top rate of 35% to a flat rate of 21%. However, to offset the reduction in corporate tax rate (and income), this act changed the rules on how research and development costs are expensed. Starting in 2022, R&D costs must be capitalized, with costs deducted over a 5-year period if the R&D activities are performed in the U.S., and over 15 years if the R&D is performed outside of the U.S. Software development is included in this new capitalization requirement. We’ll explore what this means and its impact on engineering organizations.

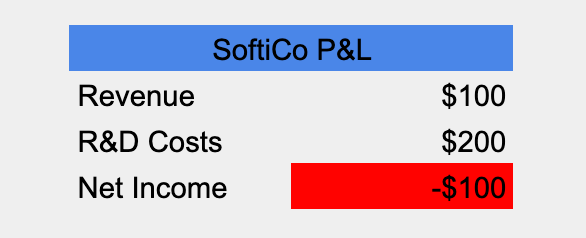

I always find it helpful to start with an example, showing how R&D costs were accounted before this rule and afterwards. Consider SoftiCo, a software company that generated $100 in revenue in 2021. SoftiCo spent $200 on software development. This spend spanned software developer salaries, tools and infrastructure costs. We’ll make an assumption that SoftiCo has no other costs, other than R&D. Therefore, its P&L statement looks like this

Because SoftiCo expensed all its software development costs ($200), it is able to register a tax loss for its fiscal year. This loss can then be used as a future tax credit. The new rule, however, changes how SoftiCo expenses the R&D costs. Rather than expense the entire $200 in one year, the new rules require SoftiCo to recognize this cost - according to some rules, which we will get into - as an asset and only expense (amortize in accounting speak) a portion of these costs in the fiscal year that they were incurred. Therefore, under the new regulations, SoftiCo’s P&L would look like so

Under the new rule, SoftiCo is only able to expense 20% of the R&D costs, while the rest is capitalized as an asset on its balance sheet. Notice how under the capitalization of R&D that SoftiCo is now generating an accounting profit, of which it now has to pay corporate income tax on. SoftiCo can no longer claim a tax credit as it was able to do when expensing all its R&D costs.

If we assume that SoftiCo’s revenue and R&D costs a year from now will be the same as the current year, then SoftiCo’s net income for the next year would be $100 - (40 + 40) = $20. Next year SoftiCo can expense the amortization of the R&D costs incurred this year and next. By year 5, and assuming all else being equal, SoftiCo’s P&L should look similar to one in which all R&D were expensed in one year.

There are a few reasons for this change. The first, should be obvious from the example above and has to do with taxation. Under the new rules, SoftiCo cannot claim a tax loss, and subsequent credit. Instead, it is liable for income tax, which the IRS gladly accepts. The second reason is profitability, multiples and valuations. One of the most common (shortcuts) to valuing companies is multiples. Some of the more common ones are P/E and EBITDA/Revenue. Prior to this accounting change, both SoftiCo’s earnings (net income) and EBITDA would be negative, rendering these multiples useless. With the new changes, the firm is profitable and therefore these multiples can be applied. I used the term shortcut deliberately, because the better way to valuations is cash flows, but I digress. For those interested, this article goes into details on this topic. The third reason argues that a portion of software development costs are actually an asset and therefore indeed to be treated as such. The software that SoftiCo develops today has a future value, which extends beyond 1 year. Therefore, similar to other assets like machines, raw material and inventory, software development costs should be captured as an asset and amortized (decayed) over time.

It’s worth noting that prior to this rule, the vast majority of software companies would expense all, or almost all of their R&D costs. Capitalizing R&D and amortizing it adds an overhead to both engineering and accounting departments, which we will get into shortly. In fact, most public software companies had a blurb similar to this one

“Software Development Costs We incur software development costs related to products to be sold, leased, or marketed to external users, internal-use software, and our websites. Software development costs capitalized were not significant for the years presented. All other costs, including those related to design or maintenance, are expensed as incurred.“ Amazon 2021 10-K

However, because of this change, many of the same software companies are adding disclaimers about the need to capitalize their R&D costs on a go forward basis. This excerpt from Facebook’s 2021 10-K (emphasis mine)

“we expect our effective tax rate for the full year 2022 to be similar to the effective tax rate for the full year 2021. This includes the effects of the mandatory capitalization and amortization of research and development expenses starting in 2022, as required by the 2017 Tax Cuts and Jobs Act (Tax Act). The mandatory capitalization requirement increases our cash tax liabilities but also decreases our effective tax rate due to increasing the foreign-derived intangible income deduction. If the mandatory capitalization requirement is deferred, our effective tax rate in 2022 could be a few percentage points higher when compared to current law and our cash tax liabilities could be several billion dollars lower.”

Earlier I mentioned that not all R&D costs can be capitalized. The costs that are eligible for capitalization are governed by accounting guidelines. This set of guidelines covered by ASC 985 and ASC 350-40 pertain specifically to software costs that a firm plans to sell or lease. These rules refer to external-use software and will be our focus. According to the accounting guidelines, you can capitalize software costs once the technology reaches technological feasibility.

“the technological feasibility of a computer software product is established when the entity has completed all planning, designing, coding, and testing activities that are necessary to establish that the product can be produced to meet its design specifications including functions, features, and technical performance requirements.”

This next section is an oversimplification on my part, consult your accounting department for guidance. Generally speaking the R&D costs that can be capitalized then are payroll costs for the engineers who are actively coding and building software that will be sold to your customers. This in turn means that bug fixes to already released software cannot be capitalized. Generally speaking, software development activities that are in service of future product enhancements are to be capitalized, whereas ones that are in service of supporting an existing product/feature cannot. Those are to be expenses. Again, this is an oversimplification, please consult an accounting expert.

The net impact of this rule is an increased burden on accounting and engineering organizations. Engineering departments must now be able to track their R&D costs to classify which of those are capitalized and which are expensed. This will require collaboration with your accounting department to first define the rules by which R&D costs are capitalized or expensed. The larger burden will be in tracking and reporting quarterly on these costs.

I found the articles below helpful for me when writing this article, and actually preparing myself to go through an R&D capitalization exercise myself.

This is a very solid and interesting post. Thank you for sharing, you can also check one of our articles https://www.metridev.com/metrics/engineering-productivity-what-is-it/

Are the ASC descriptions in the parentheses the other way around?